ICASSP 2026 · CCF B · Core A

Towards Reliable Time Series Forecasting under Future Uncertainty

Official project page

TL;DR

We improve time-series forecasting reliability under future uncertainty with ambiguity rejection and novelty rejection, allowing models to abstain from low-confidence or distribution-shifted predictions.

Authors: Ninghui Feng†, Songning Lai†, Xin Zhou, Jiayu Yang, Kunlong Feng, Zhenxiao Yin, Fobao Zhou, Zhangyi Hu, Yutao Yue, Yuxuan Liang, Boyu Wang, Hang Zhao

Overview

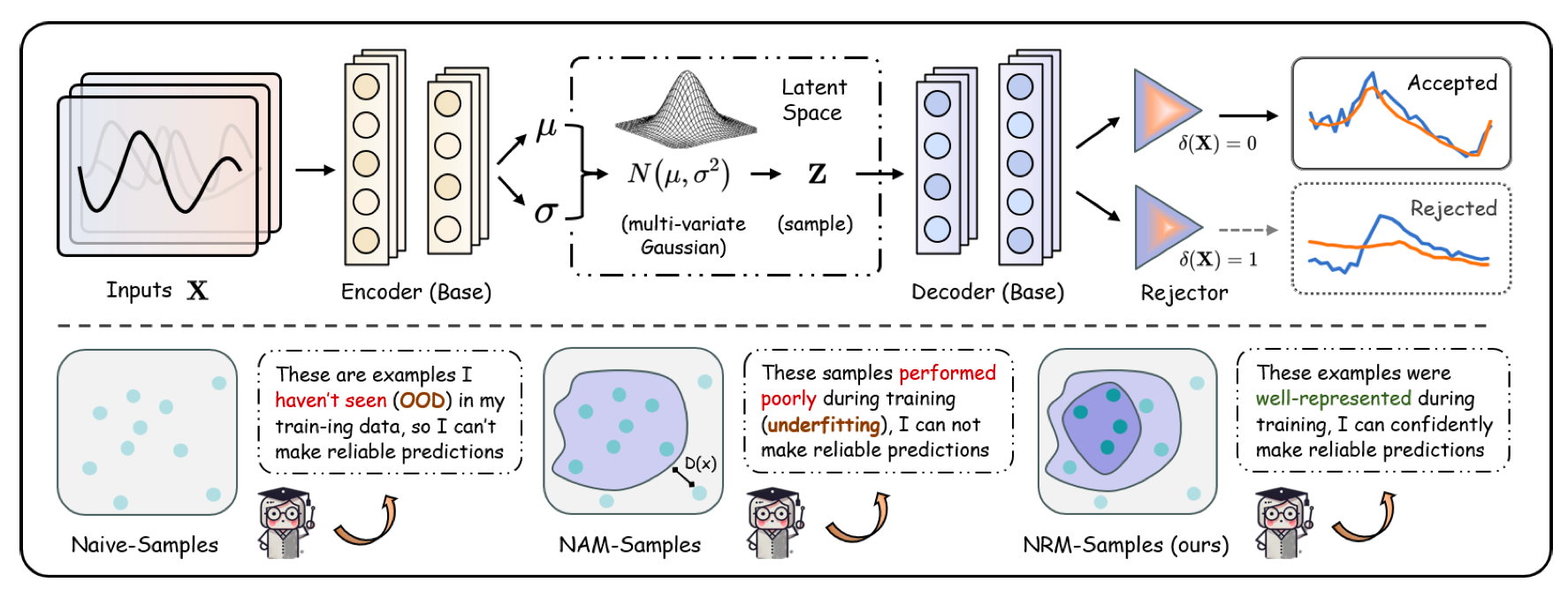

Reliable forecasting systems should know when their predictions are likely to fail. This work studies two practical uncertainty sources: ambiguous future outcomes and novel distribution shifts. The proposed framework combines ambiguity rejection based on prediction error variance with novelty rejection using representation distance, reducing risk when ground-truth future values are unavailable.

Key Ideas

- Ambiguity rejection: identify forecasts with high predictive uncertainty and abstain from unreliable outputs.

- Novelty rejection: detect out-of-distribution future conditions through representation-based distance.

- Deployment focus: reduce forecasting errors in dynamic environments without requiring future labels.